Insight

A new lens: Investing in an AI world

• 9 minute read

By Benedikt Joeris, Jonathan Wulkan, and Joris Van Gool, Partners at Hg

For more than two decades, Hg has invested behind a conviction that technology will continue improving professional productivity. Across successive waves of innovation, from on-premise software to the cloud, the pattern has been consistent. A new capability arrives, it gets absorbed into the workflows that run businesses, and the companies that master that absorption create durable customer value.

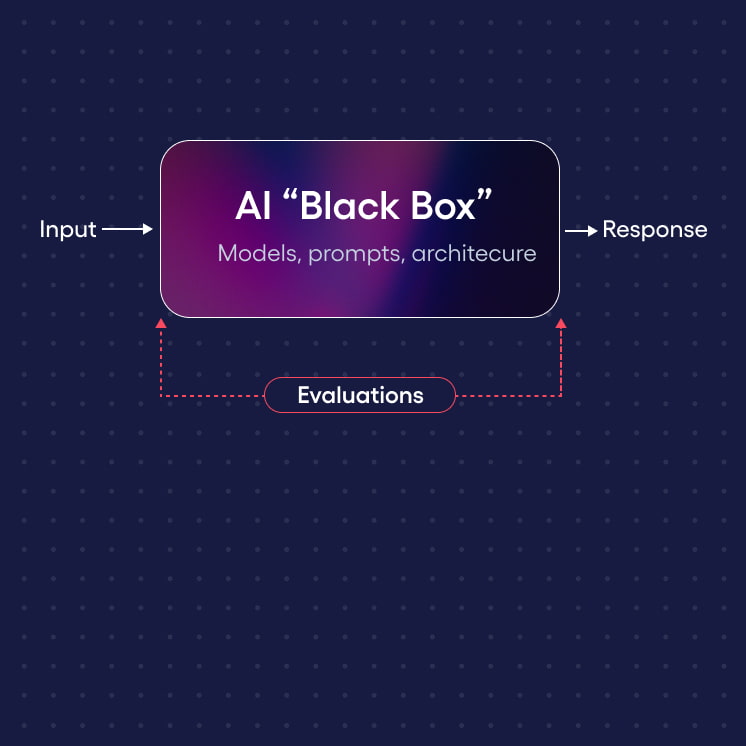

Artificial intelligence (AI) is the latest of these waves. Software is no longer confined to recording, recalling, and organising information, or executing deterministic tasks. It can now automate much more, with agents doing some of the work itself. It brings analysis, reasoning, and action. As a result, the addressable opportunity is now meaningfully larger than it was just a few years ago, creating a new ‘agentic TAM’ to go after.

Our strategy has long been focused on companies that provide mission-critical software, services, and data to professionals in complex, often regulated industries such as accounting, payroll, compliance, healthcare, and financial services. Doing this successfully requires deep domain knowledge. Accuracy is non-negotiable. Customers depend on our companies’ products to keep their businesses running, and the customer relationship, once established, tends to endure. That focus has not changed, and AI enhances it.

But we're also asking a new question. Who has the best foundations to go after the agentic TAM created by AI? Matthew Brockman has talked previously about the 'four Ds' (Domain, Data, Distribution, Deterministic), which provide a strong foundation for identifying those future winners. As we continue to make investment decisions, we've enriched this framework to build on our continued learnings.

The capital we have deployed and will over the next few years should benefit from this TAM expansion for a decade or more. While much of our strategy of the past two decades will continue to serve us well, we are now weighting four criteria more heavily than ever. They are informed in large part by the successes we are already observing across our portfolio of ~60 portfolio companies, who are actively shipping agentic AI for business customers in the “real world.”

1) World-class, product-led leadership.

Product-led leadership and product-led growth were always important. They are now decisive. The pace of change and bar for innovation our customers expect has never been higher, and leaders who possess a deep understanding of the needs for their customers will be the ones to build valuable, agentic products that those customers want to adopt.

The category leaders of tomorrow will rethink what is possible when harnessing AI in a practical way, not incrementally optimise a tired product. Leaders who embrace this change and who possess deep domain and customer understanding will thrive. The best AI strategies in our portfolio have come from companies that started from genuine product strength. They understand the intricate details of their customers' workflows, speak their language, and when they build AI into the product, customer adoption is frictionless.

Take P&I, which we first backed in 2013. It continues to grow revenue at more than 20% because its leadership has consistently invested ahead of the technology curve building world class payroll and HR solutions specifically tuned to the German market. IFS, a leader in industrial AI, is another great example. It has translated deep industrial expertise and years of in-the-field knowledge into substantial, applied AI products. Or Blinqx, where a group of product-led founders develop innovative software for regulated professions in the Benelux, understanding better than anyone else what their customers need next.

In each of those cases, leadership understood early that AI needed to be embedded in customer workflows, not tacked on as an afterthought. It becomes a natural part of product management and strategy.

2) Deep product logic in “verticalised” use cases.

We have always believed the most important structural question about a technology business is how deep its product logic runs. Every technology business encodes domain knowledge into its product in the form of rules, processes, regulatory frameworks, and accumulated operational expertise. When that logic is deep and constantly evolving, it is genuinely hard to replicate.

Consider a multi-jurisdiction, always-on tax and accounting compliance platform. It doesn't just store filings. It encodes jurisdictional rules, tracks regulatory changes in real time, and has learned from millions of prior submissions which edge cases require human review. That accumulated knowledge, trust, and domain expertise is the product. It took decades to build, and it compounds with every customer interaction.

OneStream, Lucanet, and Prophix illustrate this depth of domain for the financial intelligence layer. They provide their solutions to some of the world's most complex enterprises, encoding consolidation rules, intracompany eliminations, and regulatory frameworks across hundreds of entities and multiple jurisdictions. These are complex, deterministic problems that must be delivered at 100% accuracy, 100% of the time.

In the world of Quality Management, Health & Safety and Environment (QHSE) software, customers expect strict adherence to complicated rules across industries and geographies. Ideagen, as a leading global QHSE platform, is relied upon daily for audits, regulatory reporting and standards assessments.

What makes the logic embedded in these tech platforms valuable is not just its depth but its character. It reflects decades of interpretive judgement, how a regulation applies to a particular client, how an edge case should be handled, what the exception process looks like. And because the underlying rules change constantly, as new regulations, jurisdictions, and standards emerge, that knowledge keeps growing. Each update cycle makes the product more accurate, more trusted, and better positioned to build AI capabilities on top, which reinforces the competitive position. It positions that business to build the agentic products that capture the opportunity ahead. Vendors with deep vertical product logic should get excited every time the foundation models get better.

3) Delivering critical outcomes where the cost of failure is high.

Deep product logic tells you what's inside a business. This criterion is about what's at stake on the other side. In many of the verticals we focus on, the software's output is the outcome itself: a submitted annual report, a payroll run, a compliance certification, an audit. If the output is wrong, the consequences are immediate and often irreversible. A regulatory penalty, a missed obligation, employees not getting paid, goods not moving across borders, physical assets that do not receive a required service.

The professionals and organisations who use our software are accountable for those outcomes. An accounting firm is accountable to its clients and their regulators. A corporation running payroll is accountable to its employees and tax authorities. They choose their software for the reassurance that the outcome will be correct.

A-LIGN, where we recently invested, is a leading issuer of SOC 2, ISO 27001, Fedramp, CMMC and other cybersecurity compliance assessments globally. Its customers stake their own compliance and reputation on the accuracy of every assessment. That's the kind of outcome where customers don’t want to experiment. They value a proven, trusted provider.

The opportunity is significant. In these verticals, the volume of work typically exceeds available professional capacity. AI that meets the accuracy bar lets the professional do significantly more: a tax adviser handling twice the caseload, an auditor reviewing three times the documentation, a cyber-compliance expert completing more assessments without compromising the quality each client depends on. That expands revenue per customer rather than just protecting it.

4) Proprietary data that is created, not assembled.

The criteria above describe what a business does, who it serves, and the standards it must meet. Proprietary data is what compounds underneath all of them. Public information that once required specialised tools to aggregate is now accessible in seconds and no longer carries economic value.

To capture the agentic TAM, we look for businesses that possess a strong data flywheel created by customers using the platform, such as transaction records, operational logs, decision histories, and regulatory submissions. This is data that can't be reconstructed elsewhere and creates a valuable edge in training agentic products on the “last mile” of complexity in their end verticals.

The strongest form of this is operational data with context. By this we mean actions taken, outcomes observed, timestamps, exception histories, and the decisions that led to each. Examples include insurance claims data with adjuster notes and litigation outcomes, industrial maintenance or version records, or financial underwriting decisions tracked against outcomes over years. Data like this feeds directly back into improving the product, creating an advantage that widens every month the business runs.

Where this kind of data sits alongside deep product logic and high-stakes outcomes, the advantages reinforce each other. The logic defines the workflow. The data makes it smarter every time a customer uses it. Together, they create the foundation for agentic products that neither could support alone.

How AI adoption varies

The above describes the most important criteria we measure against, but timing matters too. AI adoption will not happen everywhere at once. Some verticals will move faster than others and understanding the pace across different customer types and geographies is central to how we assess every investment.

Verticals, geographies and use cases that have longer adoption horizons, higher costs of failure, and rely more heavily on proprietary data for model training will benefit incumbents with those building blocks, provided they have innovative, product-led teams at the helm.

Equally, the last-mile complexity of deploying AI safely across multiple jurisdictions and professional standards makes deep local knowledge critical. Europe’s regulatory fragmentation has always been a structural advantage for many of the businesses we back. AI makes it more pronounced.

A rare moment

Not every technology business will thrive in an AI world. The pace of change means world-class, product-led leadership is now a pre-requisite. It is what allows a business to build agentic products, capture new parts of the workflow, and expand what it can do for customers. But speed without foundation is fragile. It needs to be matched with deep product logic, accountability for critical outcomes, and proprietary data that compounds through usage. These are structural advantages that deepen rather than erode as AI advances. Product leadership allows you to move quickly. But you need a strong core to keep building on.

Even then, finding the right businesses is only half the equation. The other half is helping them capitalise on these advantages. Hg has spent more than a decade building the capability to accelerate this. Our Value Creation team, including more than 150 AI professionals and a dedicated AI product incubator in Hg Catalyst, works directly with portfolio companies to drive product innovation and operational transformation.

Momentum is building. We've now launched more than a hundred AI products across the portfolio, generating growing revenue. Operational AI is producing meaningful margin gains in the businesses furthest along. Product build times have compressed from nine months to under three. Companies that moved early are seeing a quarter or more of new bookings from AI products.

We're still early, too. The next five years offer more opportunity to create value in technology than the last ten. The combination of deep sector expertise, scaled operational capability, and a portfolio already generating real AI-driven results give us deep conviction. Our job now is to identify the right businesses, invest in them, and help them move faster than they could alone.

For specialist investors like us, this is a rare moment and an incredibly exciting time. We intend to make the most of it.

Disclaimer

This document does not constitute an offer to sell any securities or investment advice or recommendation, and should not be construed as research. It discusses broad market, industry or sector trends and general economic, market or political conditions only.

None of Hg or its affiliates makes any representation or warranty, express or implied, as to the correctness, accuracy or completeness of this document, which is subject to further amendment, review and verification. No responsibility or liability is accepted for updating any information contained herein, correcting any inaccuracies, or providing additional information. To the maximum extent permitted by law, Hg shall not be liable for any direct, indirect or consequential losses arising from reliance on this document.

Certain information, including forward-looking statements, economic and market information and portfolio company data, may have been obtained from published third-party sources and has not been independently verified. This document is subject to material updating, revision and amendment.

All statements of opinion, projections, forecasts and discussion of past performance represent Hg's own assessment as at the date of this document and are subject to change without notice. Any projected or target returns are hypothetical and illustrative only, and do not constitute a forecast. They are based on current views, estimations and assumptions that may require modification as economic and market conditions develop, and industry experts may disagree with them. Neither Hg nor any of its affiliates assumes any duty to update any forward-looking statement.

The value of investments and the income from them can go down as well as up, and you may not get back the amount originally invested. Past performance is not a reliable indicator of future results.

Related Articles