Built to last: why a narrow focus is the secret to Hg’s success

• 10 minute read

By Carmela Mendoza (PEI)

In May 2023, Private Equity International profiled Hg as the cover story for that month's magazine. Read the original article here

The Japanese philosophy of kaizen – a constant focus on improvement – will be key to replicating software specialist Hg’s success over the coming decades, writes Carmela Mendoza

At a general meeting in 2019, Nic Humphries, senior partner and executive chairman of software specialist Hg, told the crowd: “We don’t wish a recession on anyone, but if there is one, we feel very well prepared.”

A London-based placement agent tells Private Equity International that this is one of their stand-out memories of the firm. They note that Humphries added: “In some ways, we think you can distinguish us more because we are defensively minded as an investor.”

Humphries’ comments portray

a self-reflective and highly productive

work philosophy – one that has

turned Hg into Europe’s most active

tech investor, with more than $55 billion

under management as of the end

of March.

The London-headquartered firm’s

forte is buyouts of software and services

businesses. It is especially dominant

in the decidedly niche – and rapidly

growing – world of software-as-a-service-

enabled businesses that have

a high proportion of recurring and

contracted revenues from loyal customers.

These revenues are based on products, backed by intellectual property,

that are business critical and low

spend.

An Hg insider tells PEI that the firm calls this the “leaky bathtub” model. In essence, it’s a revenue model analogy, where most companies Hg owns start each year with over 90 percent of revenue already contracted – a feature of the SaaS software business model. That’s opposed to, for example, a consulting firm that starts each year with 0 percent revenue contracted.

“Their businesses are the kinds of software solution that customers can’t really turn off,” the insider says.

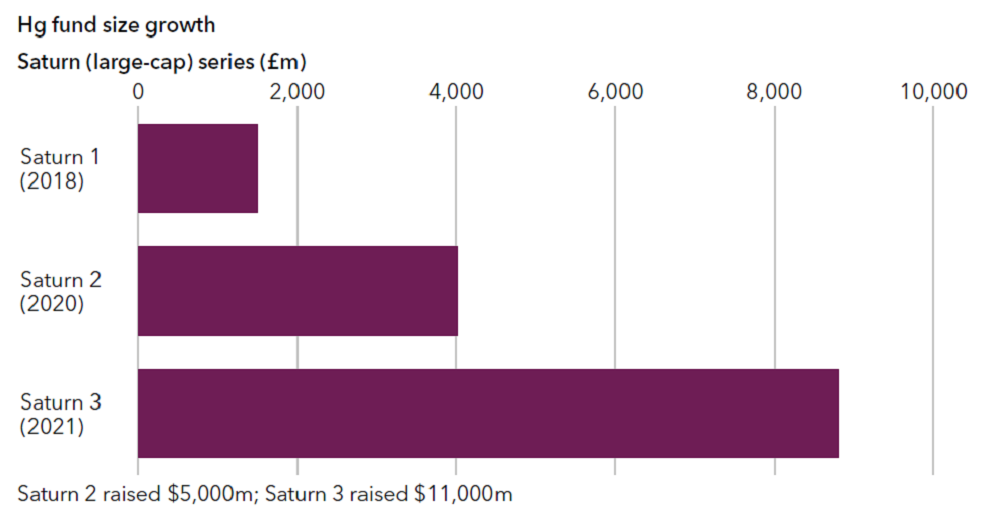

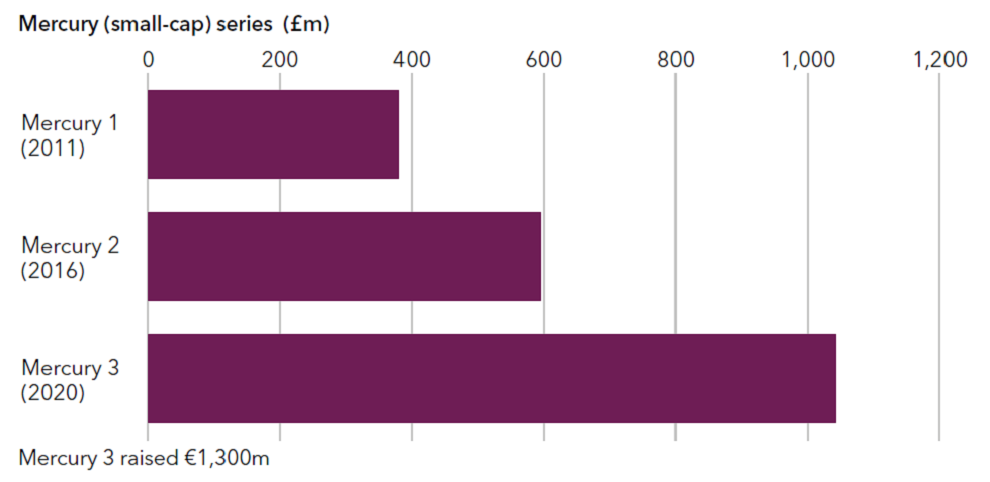

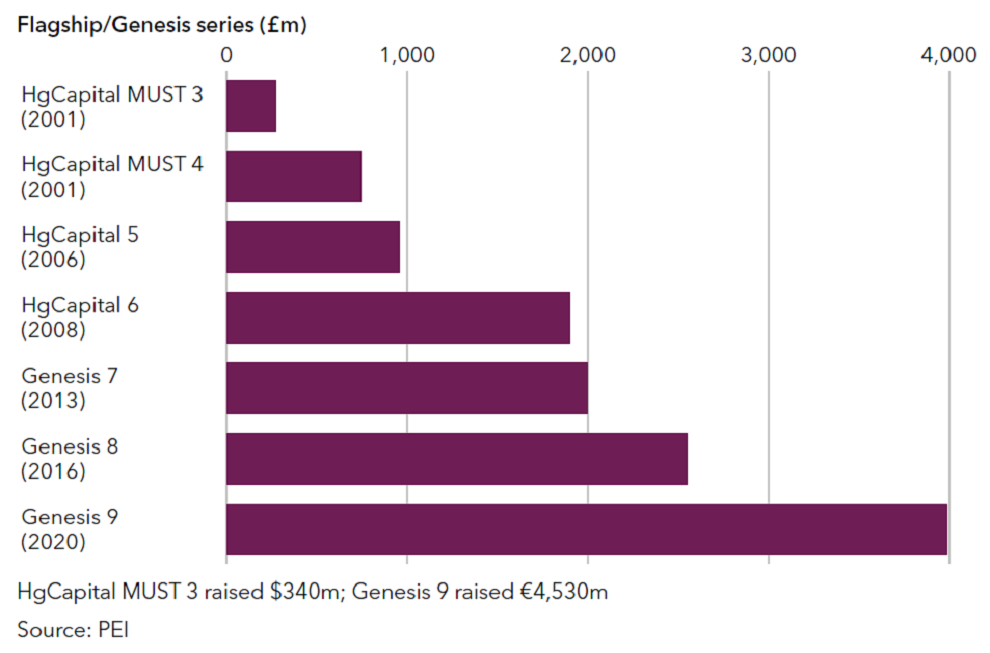

That prowess has allowed Hg to amass $11 billion for Saturn 3, its latest large-cap offering – more than double the $5 billion accrued by its 2020-vintage predecessor. It also reached the €6.75 billion hard-cap for Genesis 10 in mid-April, it is understood, and is yet to hold a final close. Funds under management have grown to over $55 billion, making it the largest UK-headquartered firm in our 2022 PEI 300 ranking of private equity’s biggest fundraisers over a five-year period. Hg can cover the entire market of software companies by having its three funds – large-cap-focused Saturn, mid-market fund Genesis and small-cap vehicle Mercury – active. Despite fundraising challenges during the height of the pandemic in 2020, it gathered $11 billion across a triple fundraise, with all three funds hitting their hard-caps.

Fund Management prowess |

|---|

In addition to its narrow investment focus, Hg appears to be

thoughtful about fund management and delivering liquidity to LPs. |

Finding its niche

Hg didn’t always live and breathe

software. The firm started out as a

mid-market generalist; it was founded

in 1990 as Mercury Asset Management

and became part of Merrill Lynch Asset

Management in the late 1990s. In

2000, the partners spun the business

out of MLAM to become HgCapital,

later renamed Hg. At the time of the

spin-out, the firm targeted industrials, healthcare, services, and technology,

media and telecoms. Its earlier vintages raised between $300 million and $900

million, PEI data shows.

Industry participants with whom

PEI spoke note that Humphries masterminded

the firm’s pivot to software

and services when he took over as chief

executive from Ian Armitage in 2007.

Jim Strang, chairman of the board at

HgCapital Trust, the listed entity that

accounts for approximately 10 percent

of Hg’s total assets under management,

says:

“Nic had the vision to say, ‘Look, what I think we should do is to narrow the focus to what we are best at (software and business services) and try to [go] deeper and deeper into these areas. And the organisation supported that.”

A London-based placement agent

also notes Humphries was “a complete

pioneer in understanding the attractiveness

of SaaS” and was “miles ahead

of other people in that respect”.

Humphries initially led Hg’s TMT

team, spearheading the sale of IRIS

Software and CS Group to Hellman &

Friedman for £500 million ($621 million;

€570 million) and also the £382

million take-private of Visma in 2006.

He joined the firm in 2001 and was

previously head of Barclays Private Equity’s

IT and telecoms team.

Humphries tells PEI that the firm’s

push into software and services was

purposeful.

“We established probably about 40 percent of our business in software back in 2004-05. We had a bit of an inflection point around the end of that decade where, to be blunt, we could have chosen to be a multi-sector, generalist mid-market firm… But I don’t think [managing partner Matthew Brockman] and I have ever wanted to be 14th or 15th at anything, and there were already lots of firms pursuing that strategy very successfully." By specialising in software, the firm had a chance to be a leader. There’s obviously risks and rewards to it. But that felt more motivating and encouraging for the people who work here as well, and for our clients. That crossroads in 2009-10 was the point at which we decided we’re going to go for an exclusive strategy.”

Giselle Bright, a partner at Bregal Private Equity Partners – an investor in Hg’s Mercury and Genesis funds – says Humphries’ sharp focus is part of what makes him such a compelling investor.

“At the time we invested in them in 2012, he could explain exactly what kind of deals he wanted to go after. He was the first one in Europe really to mention recurring revenues and this kind of approach that everyone in private equity now talks about as the Holy Grail.”

As Hg sought to refine and recalibrate its focus over the years, its performance has likewise sharpened. Since 2020, the firm has been included in the HECDowJones Private Equity Performance Ranking, which lists the world’s top PE firms in terms of aggregate performance. It ranked ninth in 2022 out of more than 560 firms. Oliver Gottschalg, professor at HEC Paris Business School, says Hg has been remarkably consistent in its strategic focus even as its funds have grown.

“That speaks to an ability to deploy almost twice as much capital in deal types that have less capital chasing them.”

He cites research that suggests the persistent nature and outperformance of best-in-class managers like Hg will mean, more likely that not, that the firm will be again among the winners going forward, even as high inflation and rising interest rates weigh on the growth prospects of tech companies.

10,000 hours

Brockman, who joined Hg in 2010, likens the firm’s gradual build to that of the sporting greats.

“When somebody wins Grand Slam tournaments or the Masters in golf, you [might] think, for example, that suddenly Emma Raducanu [has] burst onto the scene. Well, actually, they’ve been practicing for the last 10 years. They’ve now shown up and they’re now visible in a way that they weren’t when they were carefully learning their craft.” Humphries adds: “It’s not as if Raducanu only played tennis a month before. She put in probably 20,000 hours by the time she won. She’d been practicing since the age of five. It’s kind of the same as us, really.”

Many are aware or have heard of the ‘10,000-hour rule’, made popular by Malcom Gladwell’s book Outliers published in 2008. The principle holds that it takes 10,000 hours of deliberate practice to achieve mastery and worldclass expertise in any field.

Humphries notes that if a young dealmaker solely does B2B, recurring revenue software in healthcare for three to five years, they can start to become a world expert. In fact, that individual might end up being one of the top 30 or 40 people in the world because they have done some 5,000 hours. “It is that kind of 10,000 hours golden effect at Hg. That’s really what we believe in.”

Hg LPs we spoke to note that

Brockman was key to operationalising

that strategy, figuring out what it

means day-to-day and then also holding

the line on it.

Brockman tells us: “If you were going

to really differentiate your firm and

you want to differentiate in software investing,

the idea was: ‘How do you get

better at this every year? How do you

compound more knowledge, more expertise,

each year?’ You start that journey

early, so by the time you’re 15 or

20 years into it – which is where we are

now – you’ve been at this a very long

time and developed a lot of accumulated

expertise. There’s no easy substitute for

the time and energy to organically build

and then keep that flywheel moving.

“It’s not something that happens

overnight or at the whim of a strategy

presentation from a consultant. It’s not,

‘We decided to suddenly get good at

this.’ It is about accumulating years and

years of effort.”

The flywheel model is based on a concept from Jim Collins’ business book Good to Great. Put simply, the idea is that companies don’t become exceptional as a result of a single invention or initiative, but rather as a result of a series of small wins that accumulate over years of hard work, at which point momentum takes over to power a sustained period of accelerated growth. Like the wheels on a car, the amount of energy a flywheel stores depends on how fast it spins, its size and the friction it encounters.

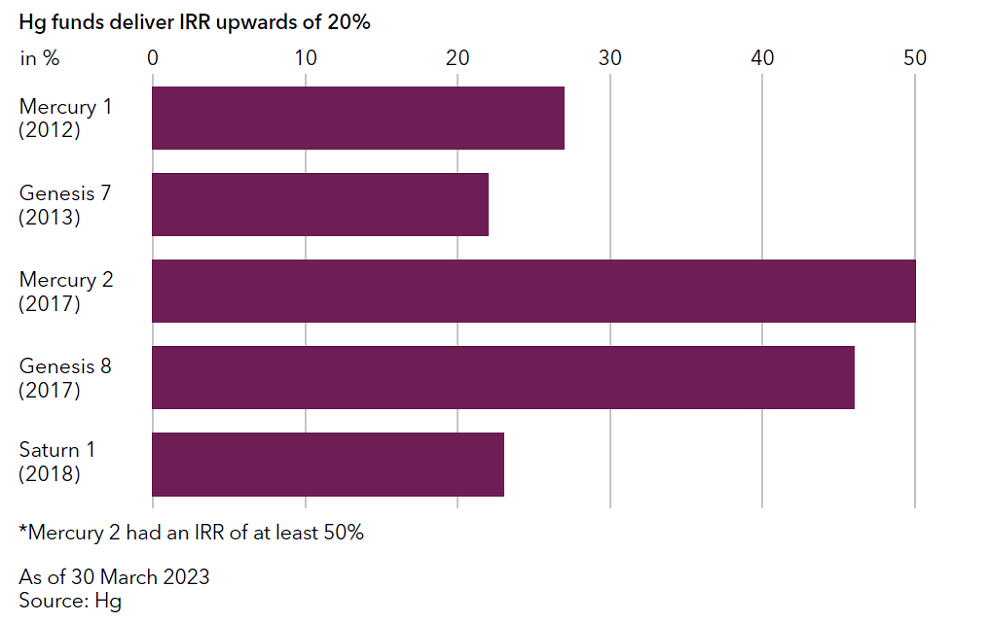

With Hg, that flywheel effect comes from investing so deeply in its eight software clusters: enterprise resource planning and payroll; tax and accounting; legal and regulatory; healthcare; insurance; automation and engineering; wealth and markets; and SME services. Needless to say, it has paid off: Hg has returned around $17 billion of proceeds to its investors at 3.3x or 33 percent IRR as of 31 March 2023, according to a factsheet on its website.

“If you don’t think about continuous improvement, you end up having to get better by 30 percent or 40 percent to catch up with the best”

Nic Humphries, Hg

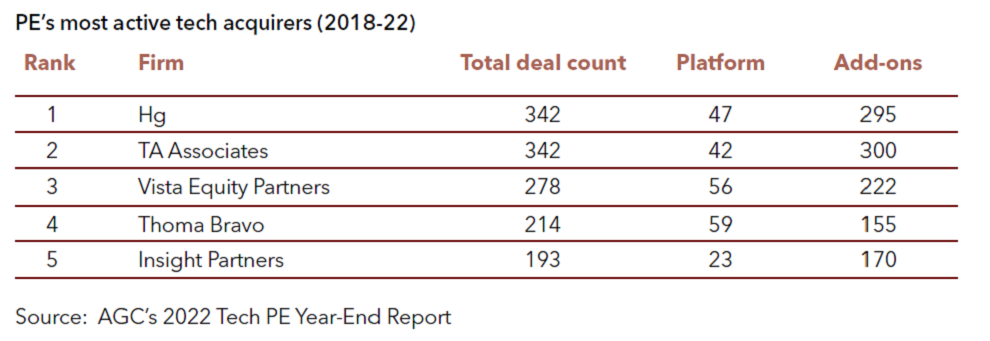

Over the past decade, Hg has backed

84 platform investments across software

and services. It was the most active tech

acquirer in 2022 with 90 transactions,

according to investment bank AGC

Partners’ latest annual report on tech PE. Alongside TA Associates, Hg was a

top tech PE acquirer by total deal count

from 2018-22, with the fi rm’s funds and

portfolio companies snapping up 342

platform deals and add-ons over the period,

according to an analysis by AGC.

“Success begets success. It’s a virtuous circle. The more success you have in a certain area, the more attractive a partner you become,” says Strang. “The more successful Hg is in a particular sort of deal archetype, the more likely it is to be deemed a suitable or preferred buyer for the next thing that comes along in the same vein. And the more that flywheel spins, the more experience Hg accumulates, and the better it gets.”

“By specialising in software, the firm had a chance to be a leader”

Nic Humphries, Hg

Visma's white knight investor |

|---|

Hg’s ownership journey with the Norwegian software firm is

a case study in how to successfully find one’s niche. |

The culture component

Culture has been critical in Hg’s success. In this regard, one Hg insider notes, the firm has a certain degree of paranoia:

“The leadership holds the line on investment discipline and [does] not let creep come in. They scaled the business very significantly, but they haven’t deviated from the core premise of what they do. It’s laudable because normally if you have so much momentum, it’s very easy to lose the rigor − to sort of start nibbling around the edges and drift into areas you know less about − to deploy capital. They are pretty hardcore on the anti-nibbling.”

Brockman says a lot of work goes into the organisational shape, culture and development of Hg’s nearly 400 employees across London, Munich, New York, Paris and San Francisco.

“We’re very team orientated. We’re very conscious of the value of a deep team,” he says. “There are probably two ways you can run businesses like ours: you can either become a real star shop, with people who are superb at finding and executing deals, and then the organisation fits around them, or you build a bank of people who can use the organisation and infrastructure and build their capability, leveraging it.”

Humphries says the firm is single- minded about embracing what it’s good at, and then doing more of it.

“If you’re great at that, focus on it and your team can support you in areas you’re not so great at. If you’re not great at something, you can go do something else and we can really support you there, and vice versa. That means we each get to do what we enjoy, which means we’ll probably continue doing it for a very long time.”

This rigour also extends to the client services team. Luke Finch, a partner at the firm who leads this unit, says:

“If we ever see people in the firm who... aren’t putting the client first, not realising who they’re working for and what we’re meant to be about, we come down on that really hard... It’s one of the things we really test for in interviewing... We inherited that real client-first mentality that goes all the way back to the founding days of Hg.”

Constant improvement

Often noted in conversations is how the firm is a believer in the Japanese philosophy of kaizen – the process of continuous improvement. The kaizen approach systematically seeks to achieve small, incremental changes in processes in order to improve efficiency and quality, whether it is at home or in the workplace.

Humphries tells us it comes back to the engineering background of a few of the figures on the top bench.

“If you can improve by 3 percent, 5 percent every year, then you don’t ever get into a situation where you’ve hit a crossroad and suddenly have to develop a strategy six years, seven years down the line... If you don’t think about continuous improvement, you end up having to get better by 30 percent or 40 percent to catch up with the best. And that’s when you take big risks, and you have a risk of failure.”

Part of this approach is constant self-assessment, where team members ask themselves the three things they weren’t good at during the year, Humphries says.

“It keeps people’s feet on the ground. And it’s amazingly humbling that even if you’re doing well, there’s loads of things you’re not really good at… That enables you to avoid doing similar deals to those that you were just lucky on.”

He points out that kaizen also extends to Hg’s relationships with its LPs, advisers and peers. “If you’re willing to accept feedback, people will tell you in a nice way. Then all you have to do is go and do it.”

The corporate culture frowns on self-aggrandisement. Apart from its Orbit podcast, which is a series of conversations between members of the Hg team and business leaders and founders, top staff do not often appear in financial media or industry conferences.

At least three of the LPs we spoke to describe the Hg team as “very down to earth” with “very low ego”. A director at an Asian investment company and an investor in Hg notes: “The firm’s self-reflective approach, based on a culture of continuous improvement, stems from Humphries and the senior leadership, and percolates down through the organisation.

“Hg was very thoughtful and deliberate in its transformational repositioning from sector generalist to sector- specialist, and what really resonates today is the consistency of personality within the firm and the clarity around its strategy… A good example of that thoughtfulness is the way they’re approaching the North America market, which several other European firms have been overzealous with – Hg [has] been very thoughtful and careful about expanding there.”

Hg added a New York office in 2019 and a San Francisco office last year. Alan Cline, a former top executive at Vista Equity Partners, joined Hg in February to lead the firm’s operations in the US and Canada. A European investor of Hg’s, who is also a member of its LPAC committee for its Mercury and Saturn fund series, adds:

“They are normal and very respectful people. They are also quite grounded and not trying to catch stars from the night sky. Being able to deal with these excellent people for me is a privilege.”

“It’s not something that happens overnight… It is about accumulating years and years of effort”

Matthew Brockman, Hg

Stopping the flywheel

The single biggest way to stop the momentum

of a flywheel is to change direction.

Hg’s senior executives say they are

well aware of this risk, and emphasised

there was real value in being disciplined.

Humphries says: “Three or four years

[ago], as other firms launched growth

funds, we were asked why we weren’t

raising for the strategy. Why aren’t we

doing crypto, venture or growing in

Asia...? We had to take a long-term

view – we were probably in about an

18-month bubble that started in March

2020 and ended in 2021 where the tech

sector was crazy – and [we] wanted to be

thoughtful [rather] than jumping into

the next fashionista thing.”

Does it bother LPs that Hg has

put all its eggs in one basket? Not at

all, four investors tell us. “They are

aggressive on their fund sizes, but the

market opportunity is there as well,”

says Bright from Bregal Private Equity

Partners. “Software isn’t going away,

and it’s even more transactional and

horizontal across the economy.”

Brockman notes that the firm is

confident that, in the next two to three

decades, the sectors they invest in will

grow at three to four times GDP, following

the tailwinds of SaaS, AI and automation. Today’s current portfolio

has more than $120 billion in aggregate

value, Humphries adds. “That’s a

lot of companies, and a lot of reach.”

“By the time you’re 15 or 20 years into it – which is where we are now – you’ve... developed a lot of accumulated expertise”

Matthew Brockman, Hg